The GEDI Institute gathers entrepreneurship and business statistics on a country’s entrepreneurial ecosystem through Global Entrepreneurship Index (GEI). In 2018 report (published in 2019), Tunisia ranked highest among all African nations included in the report, and 40th overall.

Morocco, Egypt and Algeria all appeared in the top 10 of African nations featured in the report. However, at the time the GEDI report was published start-ups in North Africa accounted for only 8% of Venture Capital funding closed across Africa.

Initiatives such as the Tunisian start-up act (launched in April 2018), and incubator programmes such as the Startup Launchpad announced by AUC Angels in November 2020 aim to further support a flourishing ecosystem. But for early-stage companies, has this support translated into growth?

North Africa VC Investment growth slows

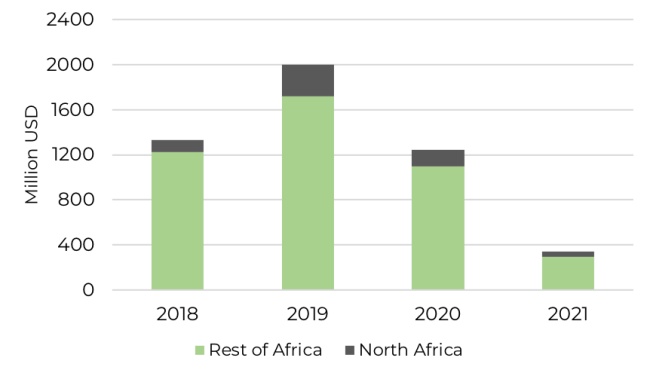

In 2018, African start-ups closed $1.331 billion USD in VC funding (excluding grants, prizes and other non-equity deals), of which start-up’s in North Africa closed $104 million USD. In 2019, the amount of funding secured by start-ups in North Africa more than doubled to $279 million USD, 14% of all venture capital funding in Africa. While funding dipped in 2020, along with broader trends across Africa, North African VC still accounted for 12% of all investment, with over $149 million USD invested.