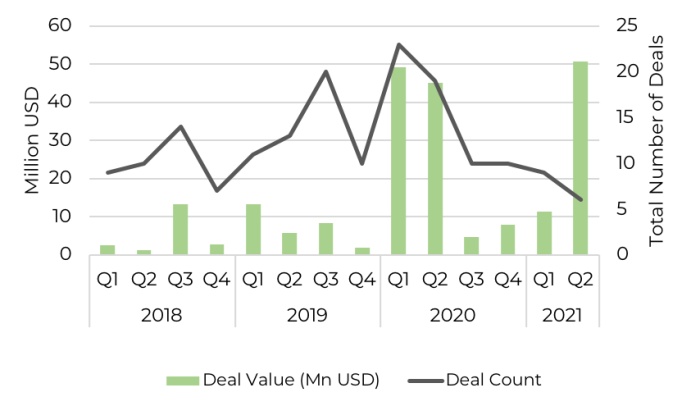

According to a report published this March by Quartz Africa, the Africa HealthTech market is booming, thanks to the increased opportunities presented by the Covid-19 pandemic. HealthTech investment reached $106.7 million USD in 2020, across 62 funding rounds, and represented 12% of all disclosed investment rounds.

A report published this week on healthcare supply chains by Salient, a healthcare advisory, noted that while many entrepreneurs in the HealthTech space express a high interest in supporting public health efforts to combat Covid-19, that the necessary commercial partnerships between industry players such as distributors, pharmaceutical manufacturers and technology companies remain limited.

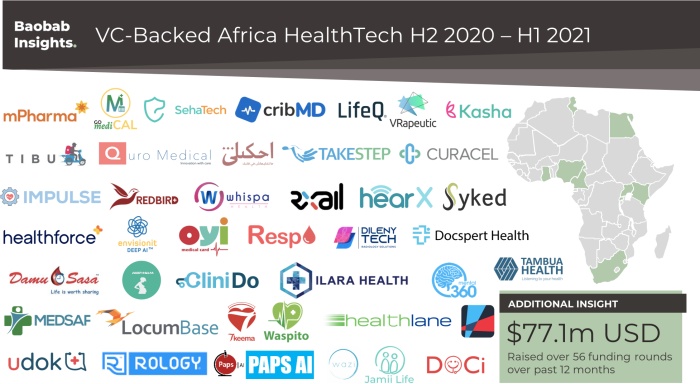

Over the last 12 months, the number of HealthTech deals has reached just over $77 million USD over 56 funding rounds. With much of this attributed to a single raise closed by LifeQ a South Africa founded biometrics company now based in United States of America.